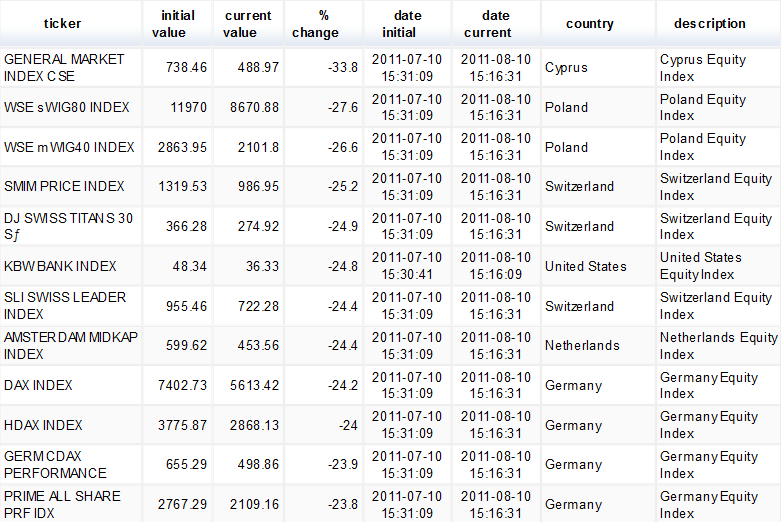

The Polish Equity Indexes WSE sWIG80 and WSE mWIG40 (which I believe are the small and mid cap equity indexes) are down 27.6% and 26.6% respectively. The more broad based WSE WIG Index is down 23.3% Here's a chart comparison of the Polish Equity Indexes that we track.

The equity decline has been happening despite the weakening of the Polish Zloty over the last 3 months. The USDPLN (US Dollar / Polish Zloty cross) has gone from 2.65 at the beginning of May to a current value of 3.00. It is now approaching the levels it was at back in January when there was some major uncertainty surrounding the eastern European economies and their level of both public and private indebtedness. Here's a chart of the % moves of several currencies from that region.

Almost all of those currencies saw a decent amount of strengthening since January but are now quickly softening again back to the January levels. We didn't even include the Belarusian Ruble, which back in June was devalued by their central bank to the tune of 66%.

Many EU banks have issued a not-insignificant amount of loans to the peripheral European economies. If those same EU banks are having issues with public and private debt within the union (see SocGen and UniCredit), then there would be even less of a likelihood of those eastern European loans being paid back at par.

No comments:

Post a Comment